MARKET UPDATE – CHINA

March 10, 2016

Canada en route to doing 1 million tonnes of barley to China this year

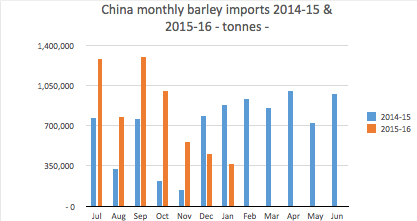

China imported a record 8.3 million tonnes (mln T) of barley in 2014-15, 4.9 mln T from Australia and 895,000 tonnes (T) from Canada, while most of the balance came from France. However the majority of the barley imports were feed quality with annual Chinese demand for malting barley imports estimated within the range of 2.5-3.0 mln T.

In 2015-16 barley imports in the first 7 months of the marketing year, from July to January, totalled 5.7 mln T. Of this 1.3 mln T came from Australia compared with 644,000 T from Canada and just over 3 miln T from France. Again much of this barley, particularly from France but also some from Australia and Canada, will be feed. But with strong demand for Canadian malting barley this year, more exports are expected with Canada en route to doing a record 1 mln T of barley to China in 2015-16, of which some 600,000 T will be malting barley, also a record.

Comparing monthly stats from last year to this year, barley imports have been considerably lower in recent months. This is likely due to a drop off in feed barley purchases as the AQSIQ in China, which provides import approvals, has tightened protocols making feed barley imports difficult. As a result, China is likely back to buying primarily malting barley for the foreseeable future.

China beer market growth curtailed

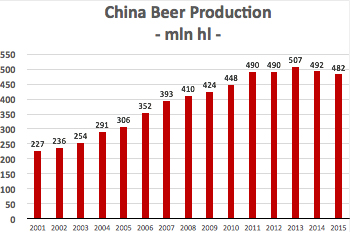

Due to rapidly increasing disposable income and growing drinking age population, China has become the world’s largest beer market by volume, while the United States remains the world’s largest beer market in terms of value. However there has been a lot of talk of slowdown in China’s brewing industry of late. After reaching over 500 million hectolitres in 2013 (one quarter of world output), production of beer in China dropped for the first time in 25 years to 492 million hectolitres in 2014, and is estimated to have fallen again in 2015 (2015 figure below is projected). A sluggish economy combined with greater interest in mid to premium quality beer has limited the absolute growth in beer volume consumed and therefore produced. In spite of this, China’s beer market remains robust and the shift to mid and premium quality beer is likely to be a boon for Canadian malting barley exports as buyers look for better quality raw materials to meet demand.

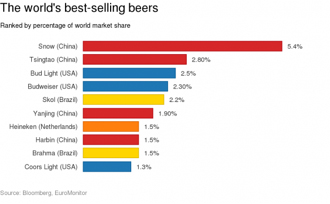

Snow beer the largest brand in the world by volume

In addition to international brewing groups such as Carlsberg and AB-InBev, China Resources Snow Breweries, Tsingtao Brewery, and Beijing Yangjing Beer are the dominant players in China. The two biggest are China Resources at 23.3 percent of the beer market in China in 2014, with Tsingtao Brewery second at 18.4 percent. Together the five big players control over 80% of the Chinese beer market. In 2014 China Resources produced 107 million hectolitres of Snow beer making it the world’s largest beer brand at 5.4% of the global market, its total volume is higher than the combined volume of Budweiser (4.6 billion liters) and Budlight (5.0 billion liters). Together with Tsingtao Brewery and Beijing Yangjing Beer, these three Chinese brewers produced 10.1% of world beer production.

The recent purchase of SABMiller by AB-InBev, to create the world’s largest beer company, will have implications for China. A deal worth over US $100 billion, the takeover is the largest in history in the area of consumer goods. However the acquisition also means SABMiller will have to divest itself of the Snow brand. China Resources picked up the brand for a bargain price of $1.6 billion, about a third of its valuation. The new brand will make China Resource by far the largest brewer in China.