GLOBAL BARLEY CROP CONDITIONS UPDATE – JULY 5, 2016

05/07/2016

The highlights of the past two weeks include firming European barley values due to concerns over disease pressure from continued rains. Meanwhile Western Canada received very timely rains and warm weather to advance crops toward an optimistic outcome. Australian barley areas have mostly received good rains with the exception of South Queensland and Northern New South Wales. Prices have been steady as there has been some Chinese demand.

Continued rains in central Europe (France) have resulted in disease issues (fusarium) and lodging of winter barley stands. There are fears that fusarium may also be prevalent in spring barley as conditions were wet during flowering. Heavy rains in Germany have also raised similar concerns. Even if the fusarium problems are not as severe as some expect, protein levels will undoubtedly be on the low side. Rains in Eastern Europe have been substantial but in a positive way as the crops are now looking good after a dry start. Spain is looking forward to their best barley harvest in years as production could hit 8 million tonnes. UK weather conditions have been positive and the barley crop is progressing well. Their market is also firming due to concerns over the French crop. Conditions in Denmark continue to be much too dry with yields now projected to be below average and protein levels higher than average. The latter point might actually be beneficial to counter the low proteins of the central European crop. Overall, farmers are hesitant sellers of new crop while the trade is looking to get some coverage.

Argentina barley seeding is in its early stages after wet weather delayed the soybean and corn harvests. We still expect the barley area will still be down dramatically as the export tax system makes wheat more attractive to grow and sell.

The Black Sea (Russia/Ukraine) barley crop is looking much better as recent warm dry conditions replaced excessive rains. The spring crop is looking especially good while the winter crop has suffered some problems.

Conditions continue to be excellent in the U.S. barley growing states. Crop advancement exceeds the five year average and the crop ratings have a high percentage in the “good to excellent” category. Rainfall amounts have been ideal and the irrigated areas have sufficient water supplies.

Western Canada has received very beneficial rainfall and relatively warm temperatures which have advanced the crop. Private production forecasts have increased the crop size to near 9 million tonnes. A large percentage of the crop is now classified as good to excellent. Domestic feed barley values have been steady as pasture conditions slowly recover.

Malting barley supplies tight in Australia & Canada

25/04/2016

Malting barley supplies in Australia are relatively tight this year given smaller than average selection rates from the 2015 crop. A dry, hot finish during last year’s harvest negatively impacted crop quality. Currently conditions are quite dry in Australia which may favour barley plantings over other crops such as canola.

In Canada there will be virtually no malting barley carry over this year after two consecutive years of poor harvest weather resulting below average supplies in both 2014 and 2015. However Statistics Canada recently projected barley area to rise in 2016, likely the result of good expected returns for malting barley, though many areas in Western Canada are dry with rains needed in coming weeks.

In the EU malting barley supplies are sufficient given last year’s large crop, although some lower grades may have been absorbed into the feed barley market where strong export sales have narrowed the premium for malt quality. Barley export licenses issued by the EU reached 8.1 mln tonnes last week, 1.2 mln tonnes ahead of last year. Spring seeding is advancing well and the winter crop is in good condition.

In the US, a large carry over from last year’s excellent crop has meant lower contracting this year. This will result in a smaller area seeded to malting barley with existing carry over stocks expected to make up the difference in the event of lower production. Barley seeding progress is reportedly close to the 5-year average.

MARKET UPDATE – CHINA

10/03/2016

Canada en route to doing 1 million tonnes of barley to China this year

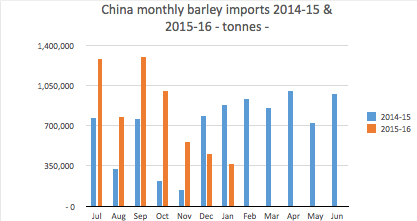

China imported a record 8.3 million tonnes (mln T) of barley in 2014-15, 4.9 mln T from Australia and 895,000 tonnes (T) from Canada, while most of the balance came from France. However the majority of the barley imports were feed quality with annual Chinese demand for malting barley imports estimated within the range of 2.5-3.0 mln T.

In 2015-16 barley imports in the first 7 months of the marketing year, from July to January, totalled 5.7 mln T. Of this 1.3 mln T came from Australia compared with 644,000 T from Canada and just over 3 miln T from France. Again much of this barley, particularly from France but also some from Australia and Canada, will be feed. But with strong demand for Canadian malting barley this year, more exports are expected with Canada en route to doing a record 1 mln T of barley to China in 2015-16, of which some 600,000 T will be malting barley, also a record.

Comparing monthly stats from last year to this year, barley imports have been considerably lower in recent months. This is likely due to a drop off in feed barley purchases as the AQSIQ in China, which provides import approvals, has tightened protocols making feed barley imports difficult. As a result, China is likely back to buying primarily malting barley for the foreseeable future.

China beer market growth curtailed

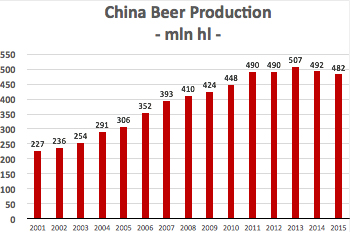

Due to rapidly increasing disposable income and growing drinking age population, China has become the world’s largest beer market by volume, while the United States remains the world’s largest beer market in terms of value. However there has been a lot of talk of slowdown in China’s brewing industry of late. After reaching over 500 million hectolitres in 2013 (one quarter of world output), production of beer in China dropped for the first time in 25 years to 492 million hectolitres in 2014, and is estimated to have fallen again in 2015 (2015 figure below is projected). A sluggish economy combined with greater interest in mid to premium quality beer has limited the absolute growth in beer volume consumed and therefore produced. In spite of this, China’s beer market remains robust and the shift to mid and premium quality beer is likely to be a boon for Canadian malting barley exports as buyers look for better quality raw materials to meet demand.

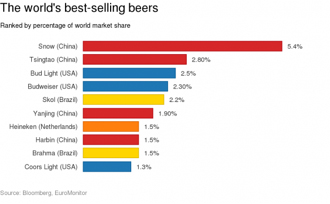

Snow beer the largest brand in the world by volume

In addition to international brewing groups such as Carlsberg and AB-InBev, China Resources Snow Breweries, Tsingtao Brewery, and Beijing Yangjing Beer are the dominant players in China. The two biggest are China Resources at 23.3 percent of the beer market in China in 2014, with Tsingtao Brewery second at 18.4 percent. Together the five big players control over 80% of the Chinese beer market. In 2014 China Resources produced 107 million hectolitres of Snow beer making it the world’s largest beer brand at 5.4% of the global market, its total volume is higher than the combined volume of Budweiser (4.6 billion liters) and Budlight (5.0 billion liters). Together with Tsingtao Brewery and Beijing Yangjing Beer, these three Chinese brewers produced 10.1% of world beer production.

The recent purchase of SABMiller by AB-InBev, to create the world’s largest beer company, will have implications for China. A deal worth over US $100 billion, the takeover is the largest in history in the area of consumer goods. However the acquisition also means SABMiller will have to divest itself of the Snow brand. China Resources picked up the brand for a bargain price of $1.6 billion, about a third of its valuation. The new brand will make China Resource by far the largest brewer in China.